Authors:

Historic Era: Era 8: The Great Depression and World War II (1929-1945)

Historic Theme:

Subject:

August 1958 | Volume 9, Issue 5

Authors:

Historic Era: Era 8: The Great Depression and World War II (1929-1945)

Historic Theme:

Subject:

August 1958 | Volume 9, Issue 5

As the twenties roared on, a market crash became inevitable. Why? And who should have stopped it?

August 1958 | Volume 9, Issue 5

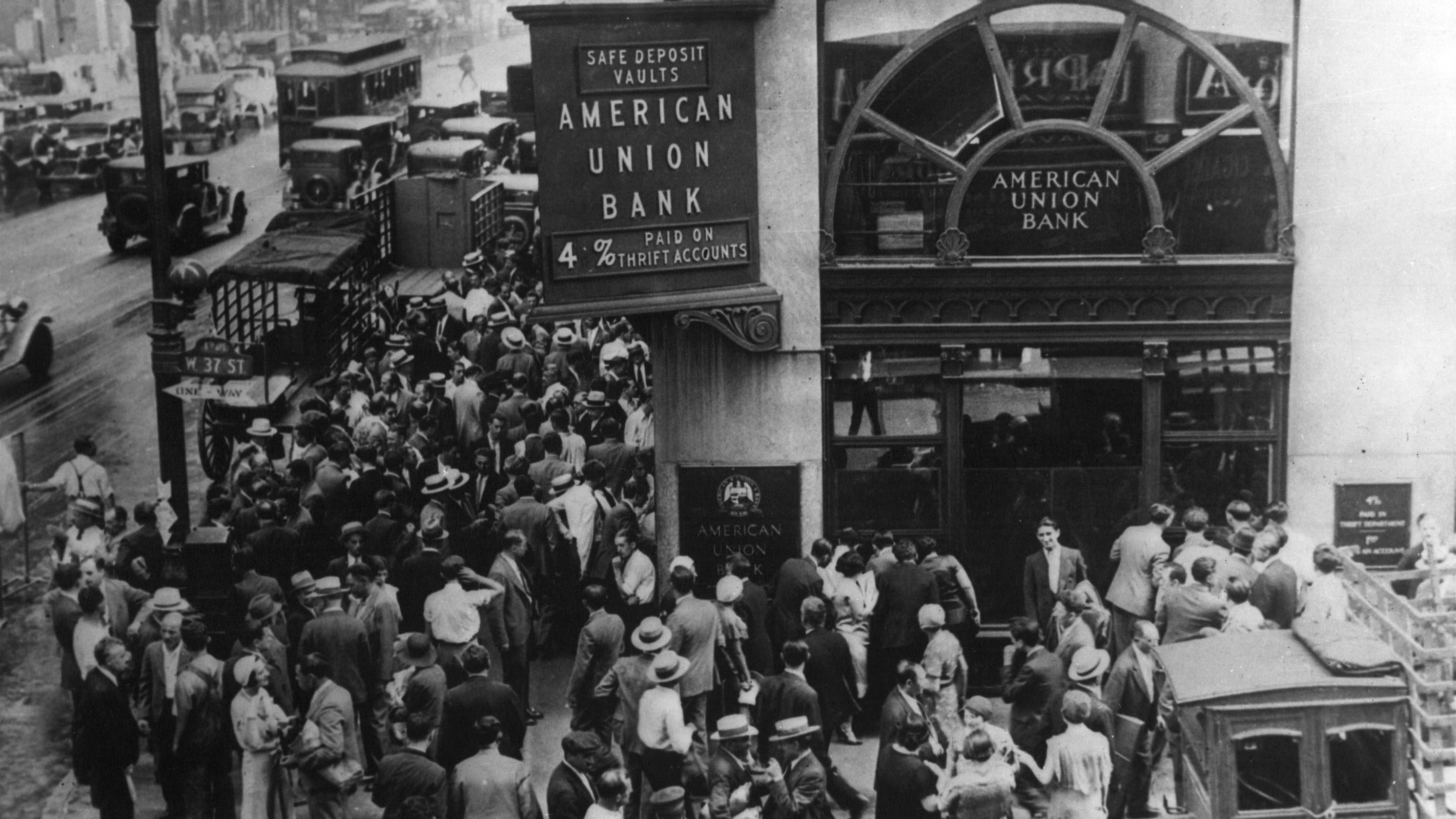

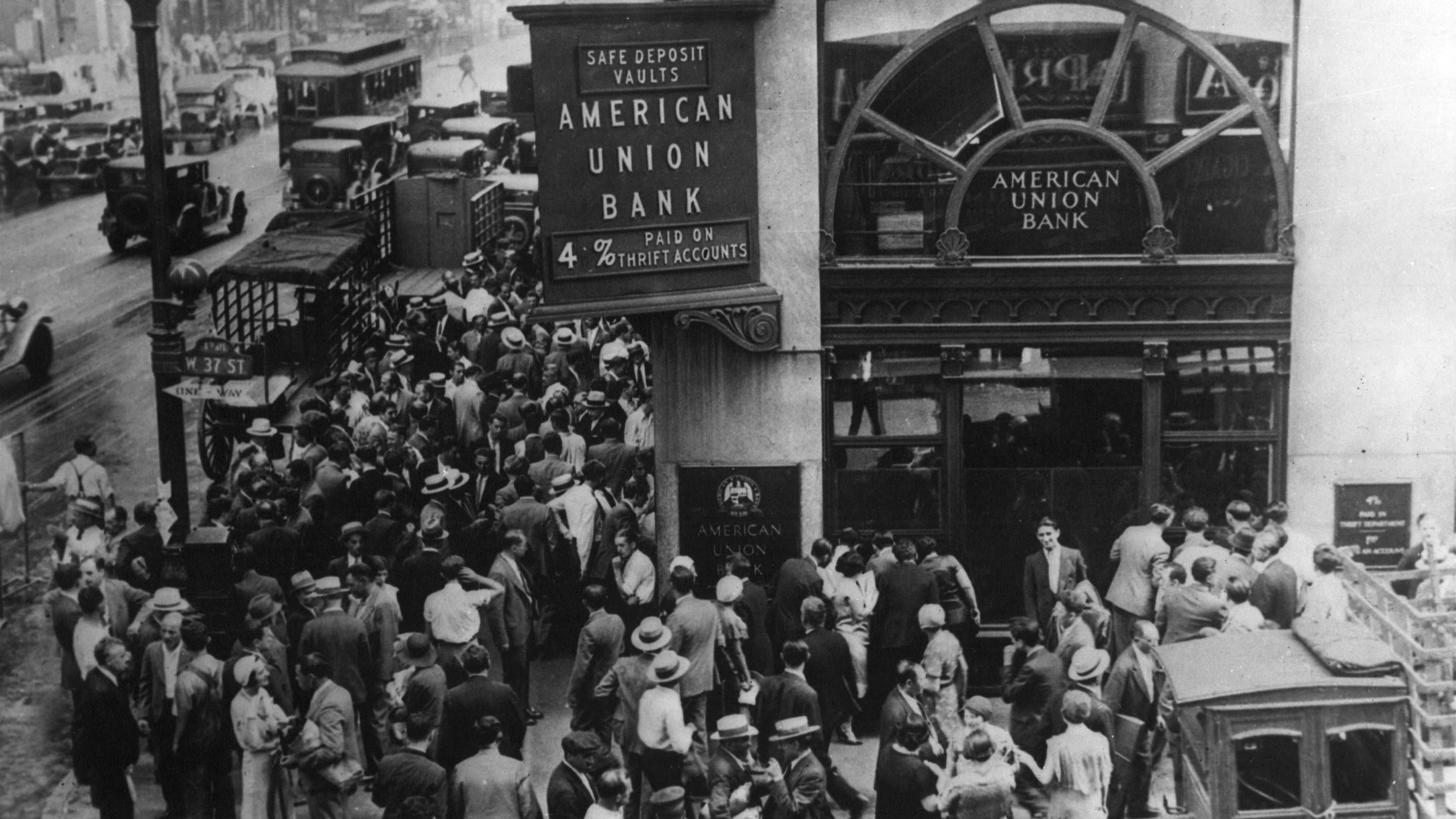

The decade of the twenties, or more precisely the eight years between the postwar depression of 1920–21 and the stock market crash in October of 1929, were prosperous ones in the United States. The total output of the economy increased by more than 50 per cent. The preceding decades had brought the automobile; now came many more and also roads on which they could be driven with reasonable reliability and comfort, There was much building. The downtown section o[ the mid-continent city—Des Moines, Omaha, Minneapolis—dates from these years. It was then, more likely than not, that what is still the leading hotel, the tallest office building, and the biggest department store went up. Radio arrived, as of course did gin and jazz.

These years were also remarkable in another respect, for as time passed it became increasingly evident that the prosperity could not last. Contained within it were the seeds of its own destruction. The country was heading into the gravest kind of trouble. Herein lies the peculiar fascination of the period for a study in the problem of leadership. For almost no steps were taken during these years to arrest the tendencies which were obviously leading, and did lead, to disaster.

At least four things were seriously wrong, and they worsened as the decade passed. And knowledge of them does not depend on the always brilliant assistance of hindsight. At least three of these Haws were highly visible and widely discussed. In ascending order, not of importance but of visibility, they were as follows:

First, income in these prosperous years was being distributed with marked inequality. Although output per worker rose steadily during the period, wages were fairly stable, as also were prices. As a result, business profits increased rapidly and so did incomes of the wealthy and the well-to-do. This tendency was nurtured by assiduous and successful efforts of Secretary of the Treasury Andrew W. Mellon to reduce income taxes with special attention to the higher brackets. In 1929 the 5 per cent of the people with the highest incomes received perhaps a third of all personal income. Between 1919 and 1929 the share of the one per cent who received the highest incomes increased by approximately one-seventh. This meant that the economy was heavily and increasingly dependent on the luxury consumption ot the well-to-do and on their willingness to reinvest what they did not or could not spend on themselves. Anything that shocked the confidence of the rich either in their personal or in their business future would have a bad effect on total spending and hence on the behavior of the economy.

This was the least visible flaw. To be sure, farmers, who were not participating in the general advance, were making